TAKING in Interest Basics

What is Simple Interest? The Basics Explained

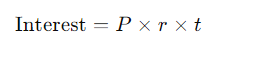

Simple interest is the quintessential form of interest calculation. It’s straightforward, predictable, and dare we say uncomplicated. Imagine you lend $1,000 at a 5% annual interest rate. Each year, you simply earn $50 in interest. Simple interest is calculated using the formula:

Where principal is the initial amount of money, rate is the annual interest rate, and time is the duration in years. This method of calculating interest is often favored for short-term loans and investments due to its predictability and ease of understanding.

How Simple Interest Works: A Quick Dive

Simple interest works like a straight line on a graph. Each year, your interest accrues based on the original principal amount, without any added complexities. For example, if you deposit $1,000 in a savings account with a simple interest rate of 4% per year, you’ll earn $40 annually. This means that over time, your interest payments stay constant, offering no surprises or exponential growth. It’s a reliable way to grow your money, though not the fastest.

Why Simple Interest is Like a Fixed-Rate Loan

Simple interest resembles a fixed-rate loan in its predictability. Just as fixed-rate loans have constant payment amounts, simple interest provides a consistent interest amount over time. This makes budgeting and forecasting straightforward, as you know exactly how much interest you’ll pay or earn. It’s like a trusty old friend who always shows up on time and never changes, no matter how much you like or dislike it.

The Wonders of Compound Interest

What is Compound Interest? Unpacking the Concept

Compound interest, on the other hand, is the financial equivalent of a magician’s hat what you see is never what you get. Unlike simple interest, which is calculated only on the initial principal, compound interest is calculated on the principal plus any accumulated interest. This means that over time, you earn interest on your interest. It’s the financial secret sauce that can make your savings grow at an exponential rate.

How Compound Interest Grows Your Money Faster

Imagine you’re planting seeds, and compound interest is the miracle grow. When interest is compounded, you’re not just earning interest on your initial investment but also on the interest that has already accrued. This creates a snowball effect, where your returns accelerate over time. For example, with a $1,000 investment at a 5% annual compound interest rate, you’ll end up with $1,051.16 after one year $51.16 more than simple interest would provide.

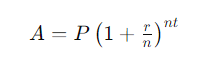

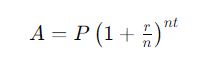

The Formula Behind Compound Interest: It’s Not Magic

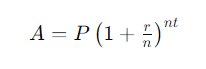

The magic of compound interest is actually rooted in a mathematical formula:

Where ( A ) is the amount of money accumulated after n years, including interest. ( P ) is the principal amount, ( r ) is the annual interest rate, ( n ) is the number of times that interest is compounded per year, and ( t ) is the time the money is invested or borrowed for. This formula showcases how your investment grows not just linearly, but exponentially.

The KEY Difference Between Interest and Compound Interest

Simple vs Compound: What’s the Big Deal?

The primary difference between simple and compound interest is how interest accumulates. Simple interest grows in a straight line, while compound interest creates a curve that accelerates over time. The key takeaway is that compound interest tends to be more advantageous for long-term investments due to its exponential growth. For short-term needs, simple interest might suffice, but if you’re aiming for maximum growth, compound interest is your best ally.

Real-Life Examples: Simple Interest vs. Compound Interest

Consider two scenarios: A savings account with a $1,000 deposit at 5% simple interest yields $50 per year, while the same deposit at 5% compound interest will yield about $51.16 in the first year. Over time, the difference becomes more pronounced. In ten years, the simple interest account would earn $500, whereas the compound interest account would grow to approximately $1,628.89. The difference underscores the power of compounding.

Why Compound Interest is the Superhero of Savings

compound interest is like the superhero of the financial world it’s all about the long game. It turns your initial investment into a growing powerhouse of returns. The more frequently interest is compounded, the greater the growth, making compound interest the go-to strategy for building substantial wealth over time. Its ability to generate earnings on previously earned interest makes it the ultimate ally for anyone serious about growing their savings.

The Impact of Compounding Frequency

Daily, Monthly, Annually: How Often Matters

Compounding frequency refers to how often interest is calculated and added to your account. The more frequently interest is compounded, the more you earn. For instance, if interest is compounded daily, you’re earning interest on your interest every single day. Monthly compounding is less frequent but still advantageous compared to annual compounding. The choice of compounding frequency can significantly impact your total returns.

The Power of Compounding More Frequently

Compounding more frequently amplifies the benefits of compound interest. Daily compounding means interest is added to your account 365 times a year, resulting in a greater accumulation of interest. Monthly or quarterly compounding, though less frequent, still offers significant advantages over annual compounding. The difference in returns might seem small initially, but over time, it can lead to substantial growth.

How Compounding Frequency Affects Your Bottom Line

To illustrate, let’s say you invest $1,000 at a 5% annual interest rate. With annual compounding, you’ll end up with $1,051.16 after one year. With monthly compounding, you’ll have approximately $1,051.16 as well, but with daily compounding, your total will slightly exceed $1,051.27. The more often interest compounds, the more money you’ll earn, proving that the frequency of compounding can be a game-changer for your finances.

Calculating Interest: A Step-by-Step Guide

How to Calculate Simple Interest: The Easy Way

Calculating simple interest is straightforward: multiply the principal amount by the interest rate and the time period. For example, if you have a $2,000 loan at a 6% interest rate for three years, the simple interest calculation would be:

This tells you how much interest you’ll pay over the life of the loan or earn on your investment. Simple, right?

How to Calculate Compound Interest: The Formula Demystified

To calculate compound interest, you’ll use the formula:

For example, with a $2,000 investment at a 6% annual interest rate compounded monthly for three years:

This formula considers how frequently interest is compounded, giving you the total amount after the specified period.

Comparing Results: Simple vs. Compound Interest Calculations

When comparing simple and compound interest, the results can be eye-opening. Using the previous examples, simple interest on a $2,000 investment at 6% over three years yields $360. With compound interest, the same investment grows to approximately $2,418.62, showing how compounding can significantly enhance returns.

The Benefits of Compound Interest

How Compound Interest Can Turbocharge Your Investments

compound interest is the secret ingredient that turbocharges investment growth. By earning interest on interest, you create a compounding effect that accelerates your wealth accumulation. It’s the financial equivalent of putting your money on a growth spurt. The longer you leave your money invested, the more pronounced the benefits of compounding.

The Snowball Effect: How Your Money Grows Exponentially

The snowball effect in compound interest means your returns grow exponentially. Like a snowball rolling downhill, your initial investment picks up momentum as interest accumulates on both the principal and the interest. This effect becomes more significant over time, turning a modest investment into a substantial sum.

Compound Interest in Retirement Accounts: Why It’s Vital

In retirement accounts, compound interest plays a crucial role. The longer your money remains invested, the more it benefits from compounding. This is why starting to save early for retirement can make a massive difference. compound interest helps your retirement savings grow exponentially, making it a cornerstone of long-term financial planning.

Common Misconceptions About Interest

Debunking Myths: Is Compound Interest Really That Much Better?

Whilecompound interest offers significant benefits, it’s not a cure-all. Some myths suggest that compound interest guarantees riches, but it depends on factors like the rate of return and time invested. Understanding its advantages is essential, but so is recognizing its limitations and the role of other financial strategies.

The Truth About How Interest is Applied

Interest can sometimes be applied in ways that seem confusing. For example, not all accounts compound interest daily, even if the promotional materials suggest it. It’s important to understand exactly how interest is applied to avoid surprises and to make informed financial decisions.

Common Pitfalls to Avoid with Simple and Compound Interest

Both simple and compound interest have pitfalls. With simple interest, the pitfall is often the lower return compared to compound interest. For compound interest, common issues include misunderstanding the impact of compounding frequency or failing to account for fees

and taxes that can diminish your returns.

Practical Applications of Interest vs. Compound Interest

How to Use Simple Interest for Short-Term Goals

Simple interest is ideal for short-term financial goals. If you’re saving for a vacation or a small purchase, simple interest accounts offer a clear and predictable return. They’re straightforward and suitable for managing short-term financial plans without the complexity of compounding.

Leveraging Compound Interest for Long-Term Wealth

For long-term financial goals, compound interest is the tool to leverage. It’s perfect for retirement savings, long-term investments, and wealth accumulation. By investing early and taking advantage of compounding, you set the stage for significant financial growth over time.

Interest in Loans: What You Need to Know

When dealing with loans, understanding interest is crucial. Simple interest loans are easier to manage and predict, while compound interest loans can be more complex. Knowing how interest is calculated and applied helps you make better financial decisions and manage loan repayment more effectively.

Strategies for Maximizing Your Returns

Smart Savings Tips to Take Advantage of Compound Interest

To maximize returns with compound interest, start saving early, reinvest your earnings, and choose accounts with frequent compounding. Regularly contributing to your investments and taking advantage of compound interest’s exponential growth can significantly enhance your financial outcomes.

How to Minimize the Impact of Simple Interest on Loans

Minimizing the impact of simple interest on loans involves paying off your loan quickly and avoiding unnecessary debt. By reducing the principal balance and paying more than the minimum, you lower the total interest paid over the life of the loan.

Planning Your Investments: Choosing the Right Interest Strategy

When planning investments, consider your financial goals and timeline. Use compound interest for long-term growth and simple interest for short-term needs. Tailoring your interest strategy to your specific goals ensures you make the most of your investments.

Interest in Everyday Life

How Credit Cards Use Simple and Compound Interest

Credit cards typically use compound interest, which means you’re charged interest on both your balance and any accrued interest. This can lead to higher costs if balances are carried over from month to month. Understanding how credit card interest works helps you manage debt more effectively.

Mortgage Interest: Simple or Compound? What You Need to Know

Mortgages generally use compound interest, which is applied monthly. This means your interest accumulates on both the principal and the previously accrued interest. Understanding mortgage interest can help you plan your payments and manage your mortgage more efficiently.

The Role of Interest in Personal Loans and Credit Lines

Interest plays a crucial role in personal loans and credit lines. Personal loans often use simple interest, while credit lines typically use compound interest. Knowing how interest is calculated helps you make informed decisions and manage your loans and credit lines effectively.

Tools and Resources for Managing Interest

Online Calculators: Making Interest Calculations Easy

Online calculators are invaluable tools for managing interest. They allow you to quickly calculate both simple and compound interest, compare different investment scenarios, and plan your finances. These tools simplify complex calculations, making it easier to make informed decisions.

Apps and Tools to Track Your Compound Interest Growth

Several apps and tools are designed to track compound interest growth. These applications help you monitor your investments, forecast future returns, and manage your financial goals. Utilizing these tools ensures you stay on top of your compound interest strategies.

Financial Software: How to Monitor Your Interest Earnings

Financial software offers comprehensive features for monitoring interest earnings. It allows you to track your investments, analyze your returns, and manage your finances in one place. Investing in quality financial software can enhance your ability to manage and grow your wealth.

The Future of Interest and Investments

Emerging Trends in Interest Calculation

Interest calculation is evolving with advancements in technology. New methods and tools are emerging that offer more precise calculations and better insights into interest management. Staying informed about these trends helps you leverage the latest innovations for financial success.

How Technology is Changing the Game for Compound Interest

Technology is transforming how we manage compound interest. With advanced algorithms and data analysis, technology provides more accurate and efficient ways to calculate and track interest. Embracing these technological advancements can optimize your financial strategies.

What to Expect: The Evolution of Interest in the Financial World

The financial world is continuously evolving, and so is the concept of interest. Future developments may bring new methods of calculating and applying interest, offering more opportunities for maximizing returns. Staying abreast of these changes ensures you remain at the forefront of financial management.

BOTTOM LINE: Mastering Interest for Financial Success

Why Understanding the KEY Difference is Crucial

Understanding the key difference between simple and compound interest is crucial for effective financial planning. It helps you make informed decisions about investments, savings, and loans, ultimately leading to better financial outcomes.

Next Steps: How to Apply What You’ve Learned About Interest

Apply your knowledge of interest to optimize your financial strategies. Use simple interest for short-term goals and compound interest for long-term growth. By understanding and applying these concepts, you can enhance your financial success.

Final Thoughts: Making Interest Work for You

Making interest work for you involves leveraging compound interest for growth and managing simple interest wisely. By understanding the dynamics of interest and applying sound financial strategies, you set yourself up for a prosperous financial future.

Frequently Asked Questions (FAQs)

Why Compound Interest is More Powerful Than Simple Interest

Compound interest is more powerful than simple interest because it grows at an accelerating rate. Unlike simple interest, which is calculated solely on the original principal,compound interest builds upon itself. This means that interest is earned on both the initial principal and the accumulated interest from previous periods. Over time, this exponential growth leads to significantly higher returns. The longer the investment period, the more pronounced the benefits of compounding become, turning a small initial amount into a much larger sum.

When to Use Compound Interest Formula?

Use the compound interest formula when you want to calculate the interest earned on an investment where interest is added to the principal periodically. This formula is essential for understanding long-term growth on savings, investments, and loans where the interest compounds at regular intervals such as monthly, quarterly, or annually. It helps you determine how much your investment will grow over time when interest is calculated on both the principal and any accrued interest. Source

What is an Example of Simple and Compound Interest?

An example of simple interest is a $1,000 loan at a 5% annual interest rate over three years. The interest would be $150, calculated as follows:

An example of compound interest is the same $1,000 investment at a 5% annual rate compounded annually over three years. The amount would be approximately $1,157.63, calculated using:

Where ( P ) is the principal, ( r ) is the annual interest rate, ( n ) is the number of times interest is compounded per year, and ( t ) is the number of years. Source

Which is More Expensive Simple Interest or Compound Interest?

Compound interest is generally more expensive than simple interest when applied to loans. This is because compound interest accumulates on both the principal and the accrued interest, leading to a higher total cost over time. Simple interest, in contrast, is calculated only on the initial principal, making it less costly in comparison. The compounding effect of compound interest can significantly increase the total amount repaid or earned, especially over long periods.

Are Most Loans Compound or Simple Interest?

Most loans use compound interest. This includes mortgages, auto loans, and credit card balances. Compound interest allows lenders to earn interest on the interest that accrues, increasing the total amount repaid by borrowers over time. Simple interest is less common in loans but can be found in some personal loans and certain types of short-term credit.

Is Compound Interest Equal to Interest on Interest?

Yes, compound interest is effectively interest on interest. It is calculated not just on the original principal but also on the interest that has been added to the principal. This results in interest being earned on previously accrued interest, leading to exponential growth of the investment or debt. This concept distinguishes compound interest from simple interest, which is calculated only on the initial principal. Source

Which is Better Compound Interest or Simple Interest?

Compound interest is generally better for investments and savings because it allows for exponential growth. The ability to earn interest on both the principal and previously accrued interest can lead to significantly higher returns over time. Simple interest is better for short-term loans or investments where predictable, linear growth is preferred. For long-term financial goals, compound interesttypically offers more substantial benefits.

What is the Difference Between Simple Interest and Compound Interest Calculator?

The difference lies in how they compute the interest. A simple interest calculator uses the formula:

To determine the total interest based on the principal, rate, and time. A compound interest calculator uses:

To calculate the total amount including interest, based on the frequency of compounding. The compound interest calculator accounts for the interest that accrues on previously earned interest, while the simple interest calculator does not.

What is the Difference Between Simple Interest and Compound Interest Sum?

The sum of simple interest is calculated as:

Whereas the sum of compound interest is calculated as:

The compound interest sum includes the principal plus interest accrued on both the principal and previously accumulated interest, leading to a larger total sum compared to simple interest over the same period and rate.

What is the Difference Between Compound Interest and Fixed Interest?

Compound interest refers to interest that is calculated on both the principal and any accumulated interest. Fixed interest, on the other hand, remains constant over the life of the loan or investment. The term “fixed interest” typically describes the interest rate itself, while “compound interest” describes how the interest is calculated and accumulated. Compound interest can vary depending on the frequency of compounding, whereas fixed interest remains unchanged.

How to Calculate Compound Interest Formula?

To calculate compound interest, use the formula:

Where:

- ( A ) is the amount of money accumulated after n years, including interest.

- ( P ) is the principal amount (the initial sum of money).

- ( r ) is the annual interest rate (decimal).

- ( n ) is the number of times interest is compounded per year.

- ( t ) is the number of years the money is invested or borrowed.

Is Interest Compounded Monthly or Yearly?

Interest can be compounded either monthly or yearly, depending on the terms of the investment or loan. Monthly compounding means interest is calculated and added to the principal every month, resulting in more frequent accumulation. Yearly compounding means interest is calculated and added annually. The frequency of compounding affects the total amount of interest accrued over time.

What is the Formula for Interest?

The formula for simple interest is:

For compound interest, the formula is:

Where ( A ) represents the total amount, including interest, for compound interest. Each formula is used depending on whether simple or compound interest is being calculated.

What is an Example of a Compound Interest?

If you invest $1,000 at an annual interest rate of 5% compounded annually for 3 years, the amount after 3 years would be calculated as:

The compound interest earned would be $157.63, illustrating how interest accumulates on both the principal and the interest earned over time.

What is Compound Interest Also Known As?

Compound interest is also known as “interest on interest.” This term reflects the fact that it involves earning interest on previously accumulated interest, leading to exponential growth of an investment or debt. The term emphasizes the compounding effect that differentiates it from simple interest.

{kind=link}